Ben S. Bernanke is an acclaimed authority on the causes of the Great Depression. From the very beginning of his career, he’s been seen as an expert in the causes of the long financial crisis following the 1929 Crash. He’s a leading expert on, among other things, efficient markets for assets of bankruptcy and foreclosures.

That’s good. Perhaps, he understands the essential goodness of the foreclosure that claimed his boyhood home in Augusta, Georgia. When asked to comment on that, the Chairman declined, except to say the Fed needs to "stimulate demand". Perhaps, he might clarify for us what he means by that?

When he was nominated as Fed Chairman in 2006, expertise in Depression-related economic theory was held up as a strong selling point.

We are starting to see the point.

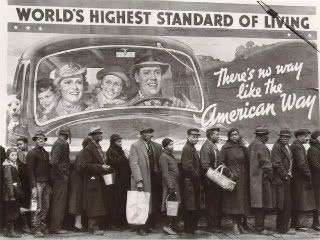

If Bernanke's appointment was meant to avoid the onset of Depression-like conditions, and the human suffering of joblessness, personal ruin and foreclosures, he has failed. Miserably. He has done precious little to push the banking industry to implement even the modest tools Congress made available to help distressed homeowners, or to seek stronger measures to modify mortgages. But, if he was brought on to merely manage the financial crisis for a banking industry that seeks consolidation after a high-risk, high-profit binge of bubble speculation, mergers and acquisitions, he may be perfect for the job. There’s a big difference in emphasis there, and the two talents should not be confused.

Ben Bernanke seemed like the right pick for Bush in 2006. He may not be the right man for the job to assist President Obama in preventing or mitigating another Depression.

In Bernanke's book, the Great Depression wasn't really the result of crashing markets, shuttered factories, and millions of homeless. No. The problem was that markets for liquidated assets of bankruptcies and home foreclosures weren't sufficiently "efficient" in the 1930s. Not efficient way back then, of course, but we know much better now about how to keep markets operating, don't we?

No wonder we're in this mess, again. No wonder Bush picked Ben Bernanke to succeed a fleeing Alan Greenspan.

Ben Bernanke made his name as an economist after he published a paper about the role of bankruptcies in recessions. In the June 1983 American Economic Review, the future Fed Chairman stated that a major reason the 1929-33 recession turned into systemic bank failure and a Great Depression was that bankers didn't have enough information about the returns they could realize from liquidating customer assets. In consummate economistese Bernanke wrote:

The present paper builds on the Friedman-Schwartz work by considering a third way that the financial crises (in which we include consumer bankruptcies as well as the failures of banks and other lenders) may have affected output. The basic premise is that, because markets for financial claims are incomplete, intermediation between some classes of lenders and borrowers requires nontrivial market-making and information gathering services. The disruptions of 1930-1933, as I shall show, reduced the effectiveness of the financial sector as a whole in performing these services. p. 257

Here, in plainer words, Bernanke offers a nice, neat explanation for why the Great Depression lasted so long. The freeze-up in the credit markets that resulted in the March 10, 1933 "Bank Holiday" was unnecessarily protracted and severe because markets for the disposal of bankruptcies and foreclosures were insufficiently developed. Lenders, not having sufficient information about the money they could have been making, essentially stopped lending. That, he surmised, snowballed into a deep, downward spiral of industrial failure, protracted unemployment, and lowered output of goods and services.

In other words, what bankers didn't know about bankruptcy could destroy the American economy. And, it did. And, did again . . .

The solution Bernanke suggested is more up-to-date and accurate reporting of distress sales -- i.e., a well-managed recession under all-seeing Fed supervision. No need for any fundamental reforms in banking practices or intervention to assist homeowners. The market is perfect, bankers are rational, and with enough information they will surely correct themselves.

Bottom line, the Fed Chairman thought that jobless recovery and the mortgage crisis were quite manageable (not a real problem) and that the answer was an efficient reporting system and market for foreclosures. Bernanke believed a prolonged Depression was impossible regardless of how many people were put out in the street, provided bankers were sufficiently well-informed about the details and markets for foreclosures continued to clear and operate efficiently. Prices will drop, lives will be ruined, but that’s simply the way the system works. Prices can be stabilized, Bernanke said in 2006, by "helicopter dropping" money into the wreckage. That is a technician’s eye view.

Ben, you're a great humanitarian, and a great economist, and perhaps a good helicopter pilot. But, try to explain your concepts of rational markets, and imperfect information to the six million Americans who will be homeless by the end of the year. That will happen because of your policies, and lacking a strong voice at the Fed advocating reforms in bankruptcy and foreclosures, because Congress will continue to drag its feet in granting relief to distressed homeowners. Recently, the Chairman has signaled support for some mild forms of mortgage relief, but it seems a case of far too little, too late. While immensely knowledgeable about the technical problems of markets and banking during the Depression, in the here and now the Fed Chairman has failed to take a leading role in advocating deep financial reforms needed to deal with the economic crisis.

Even Greenspan admitted he was wrong in his fundamental assumptions. What about you, Mr. Bernanke? Where’s your public moment of awful realization?

The problem with Chairman Bernanke is not that he's a supply-sider, or a right-wing ideologue, or too close to Bush, it is that he is thoroughly conventional American economist. An exemplary American economist, a complete professional, and if he showed himself to be anything else, it is unlikely that he would have gotten anywhere near the top of his profession. But, that's the problem.

The awful reality that drove Greenspan from the Temple, and Lehman to ruin, is that the "real economy" of mortgages, household income, factory output, and trade in services are being destroyed by the other economy created by the global financial industry. Derivatives, mortgage default swaps, reverse repos, naked puts, and other ethereal instruments did not grow spontaneously. Someone created them, and they need to be held accountable. "Helicopter dropping", in Bernanke's signature phrase, another trillion dollars over Wall Street just won't do this time.

Left to their own devices, even the Fed’s Primary Dealers go crooked and make bad bets. Greenspan allowed secondary markets for securitized debt and assets-backed derivatives to grow unattended, so that they came to dwarf and drain the life out of the financial system and the real world economy. Now, even all the Treasuries in the repo market that Bernanke might helicopter drop can’t save the banks from themselves. Meltdowns happen, when you let the reactor run critical on its own.

Efficient bankruptcies and interest rate drops won’t prevent catastrophies, Mr. Chairman. Negative real interest rates can be counter-reproductive, locking up secondary markets. That happened in September with the repo market, killing Lehman Bros. Look at Japan in the decade of the 1990s for what the fetish with interest rate drops can do on the macroeconomic level.

Bankers are greedy, rapacious and reckless, and if given their own way, will blow up economies – they’ve demonstrated that repeatedly -- particularly if there’s a fortune to be made on the down side. Some people can make money out of anything, even radioactive waste removal has value.

What is needed now at the Fed is a Bad Sheriff with a heart, not a good reactor room technician with a pilot's license.

________

Bernanke's original thinking about how Depressions can be prevented by better bankruptcies and efficient foreclosures clearly discernable by the second page of Bernanke's 1983 paper, the initial sections of which are surprisingly readable. See, Ben S. Bernanke, "Nonmonetary Effects of the Financial Crisis in Propagation of the Great Depression," American Economic Review, American Economic Association, vol. 73(3), pages 257-76, June. http://fraser.stlouisfed.org/...

Bernake would write repeatedly on the subject of the role of imperfect banking knowledge and practices in bankruptcies, settlements and clearing during the Depression. See, http://ideas.repec.org/... Here's a string of citations that shows the context of Bernanke's formative thinking on these subjects.

If there's someone out there who can show that Bernanke has fundamentally changed his thinking on this topic -- and now believes personal bankruptcies and home forceclosures are not only politically undesirable, but economically destructive, and the government should take steps be prevent them -- that contribution to our understanding would be most welcome.

___________

Bernanke's emphasis on bankruptcy is clearly seen in the first professional paper he published two years earlier,

Barro, Robert J, 1978. "Unanticipated Money, Output, and the Price Level in the United States," Journal of Political Economy, University of Chicago Press, vol. 86(4), pages 549-80, August. [Downloadable!] (restricted)

Sargent, Thomas J, 1976. "A Classical Macroeconometric Model for the United States," Journal of Political Economy, University of Chicago Press, vol. 84(2), pages 207-37, April. [Downloadable!] (restricted)

Bernanke, Ben S, 1981. "Bankruptcy, Liquidity, and Recession," American Economic Review, American Economic Association, vol. 71(2), pages 155-59, May.

Stiglitz, Joseph E & Weiss, Andrew, 1981. "Credit Rationing in Markets with Imperfect Information," American Economic Review, American Economic Association, vol. 71(3), pages 393-410, June. [Downloadable!] (restricted)

Lucas, Robert Jr., 1972. "Expectations and the neutrality of money," Journal of Economic Theory, Elsevier, vol. 4(2), pages 103-124, April. [Downloadable!] (restricted)

Abel, Andrew B. & Mishkin, Frederic S., 1983. "An integrated view of tests of rationality, market efficiency and the short-run neutrality of monetary policy," Journal of Monetary Economics, Elsevier, vol. 11(1), pages 3-24. [Downloadable!] (restricted)

Other versions:

Andrew B. Abel & Frederic S. Mishkin, 1983. "An Integrated View of Tests of Rationality, Market Efficiency, and the Short-Run Neutrality of Monetary Policy," NBER Working Papers 0726, National Bureau of Economic Research, Inc. [Downloadable!] (restricted) Fama, Eugene F., 1980. "Banking in the theory of finance," Journal of Monetary Economics, Elsevier, vol. 6(1), pages 39-57, January. [Downloadable!] (restricted)

Douglas W. Diamond & Philip H. Dybvig, 2000. "Bank runs, deposit insurance, and liquidity," Quarterly Review, Federal Reserve Bank of Minneapolis, issue Win, pages 14-23. [Downloadble!]

Other versions:

Diamond, Douglas W & Dybvig, Philip H, 1983. "Bank Runs, Deposit Insurance, and Liquidity," Journal of Political Economy, University of Chicago Press, vol. 91(3), pages 401-19, June. [Downloadable!] (restricted)

Robert J. Gordon & James A. Wilcox, 1981. "Monetarist Interpretations of the Great Depression: An Evaluation and Critique," NBER Working Papers 0300, National Bureau of Economic Research, Inc. [Downloadable!] (restricted)

Full references[/i]